Set Up for Success, Insured: The Fiduciary Infrastructure Put in Place

By: Sam Rocke, CFP®12/14/2021

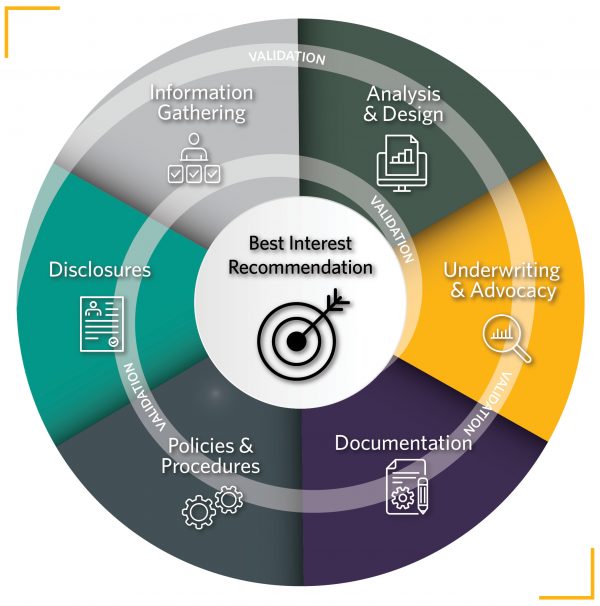

Focusing on the remaining nine key aspects of the fiduciary infrastructure, we call your attention to the importance of aligning all areas of a fiduciary practice around these standards – including insurance.

In the Set Up for Success, Insured series, our latest blog noted that modern fiduciary regulations require a solid fiduciary infrastructure before making a best interest recommendation. There are 10 components to Palladium Group’s fiduciary infrastructure, one of which — insurance company and product due diligence — were discussed in the last blog. Today, we turn our attention to the remaining nine. While most, if not all, of these are considerations a prudent fiduciary will have already incorporated into his or her practice, it bears mentioning the importance of aligning all areas of a fiduciary practice around these standards — including insurance.

Conflict management. All fiduciary regulations place management of conflicts as a primary fiduciary obligation. Some conflicts must be eliminated, while others mitigated. For Palladium Group, the conflict created by the compensation we earn is fully disclosed in our affiliated broker-dealer’s Reg BI disclosures when selling variable products. When a recommendation or investment strategy is made, it is made in your client’s best interest given their individual financial circumstances, needs, and goals.

Compliance policies and procedures. The Department of Justice (DOJ) provides guidance on the framework of a good compliance program, which comprises of design (assessment of risks, policies and procedures, training and communication, and third-party oversight), implementation (including buy-in from leaders), and demonstrated effectiveness. It is important for fiduciaries to have documented policies and procedures about their fiduciary practices.

Compensation practices. The regulations allow fiduciaries to receive reasonable compensation. Most insurance companies pay within a tight range compared to each other. Even then, any differentials must be addressed as part of conflicts management.

Surveillance and audit. Fiduciaries should have procedures to oversee transactions and test their policies at least annually. According to the DOJ, a good surveillance program should include the following basics: test, investigate, remediate, improve…and repeat.

Training. Fiduciary regulations emphasize the need for proper training of advisors before making best interest recommendations. The insurance industry has broken this down into three levels: training on the best interest standard, training on product types, and training about specific products. As your expert insurance partner, the Palladium Group team receives regular training in each of these areas.

Forms. Forms should be designed to gather the necessary client information to know your customer to determine product or strategy best for your client. This approach could mean different forms for different situations — general client intake, rollovers, 1035s, conversions, and more.

Forms management. Forms should be organized to ensure the proper documents are used.

Disclosures. Clients need to receive disclosures. Generally, regulations treat disclosures similarly, but there are notable differences between fixed and variable products. Insurance carriers typically provide the disclosures for fixed products. Insurance carriers and broker-dealers provide disclosures for variable products.

Documentation. Always document the file. There should be a description demonstrating why a product or strategy is best for the client, the application, and broker-dealer client profile (if applicable), along with supporting documentation like the illustration and product comparisons.

Palladium Group's Fiduciary Approach Model

Set Up for Success, Insured: The Series

Expanding your fiduciary knowledge alongside Palladium Group’s easy, education-oriented process adds continual value for you and your clients. As we continue to expand on more throughout the Set Up for Success, Insured series, you can have confidence your adherence to your fiduciary duty extends to all areas of your practice — including life insurance and annuities planning. Keep an eye out as Palladium Group dives into the DOL fiduciary rule enforcement, which took place on February 1, 2022.

*This material is for financial professional and educational use only. Not to be reproduced or shown to clients.